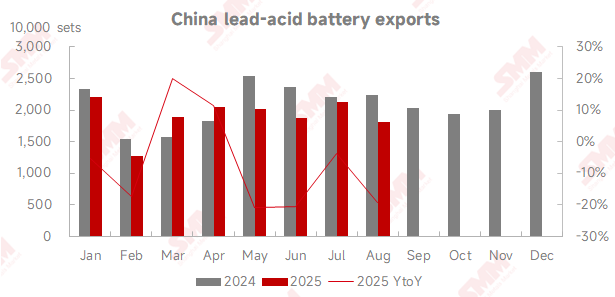

SMM, September 23: According to customs data, China's lead-acid battery exports totaled 18.1577 million units in August 2025, down 14.7% MoM and 19.14% YoY. Cumulative exports from January to August 2025 reached 152 million units, a decrease of 7.93% YoY.In August 2025, China imported 341,200 lead-acid batteries, down 13.43% MoM and 33.28% YoY. Cumulative imports from January to August 2025 stood at 3.5187 million units, declining 5.33% YoY.

In August, the SHFE/LME lead price ratio gradually widened, with domestic lead prices significantly higher than overseas markets. The monthly average export loss for lead ingots was around -2,500 yuan/mt, meaning China's lead-acid battery export costs were uncompetitive in overseas markets. Meanwhile, tariff policies such as those in the US (reciprocal tariffs) and the Middle East (anti-dumping punitive tariffs) increasingly impacted China's exports. The "export rush" orders from overseas customers' advance purchases were largely fulfilled by lead-acid battery enterprises in July. By August, exports returned to actual transactions but were weaker than pre-rush levels. Based on August export data, exports to 12 of the top 15 destinations declined MoM, including India (down 16.74%), the US (down 19.63%), the UAE (down 7.81%), and Saudi Arabia (down 65.13%). Exports to Southeast Asian countries also fell to varying degrees.

In September, the domestic-international lead price ratio expanded further, reaching levels that opened the import window for refined lead. Lead-acid battery export pressures multiplied, and with ongoing tariff impacts, September exports are expected to weaken further. According to feedback from lead-acid battery enterprises in Zhejiang, Guangdong, and other regions, domestic lead prices have fluctuated upward since Q3, raising production costs. Combined with tariff policies, export orders have continued to decline. Currently, operating rates are maintained at only 50-70%, with some enterprises even below 50%.